The bill arrives

We have entered a new climate phase: The Bill Arrives. To see how we got here, walk with me through the earlier phases, and how rules, money, and everyday life have shifted over the last few decades.

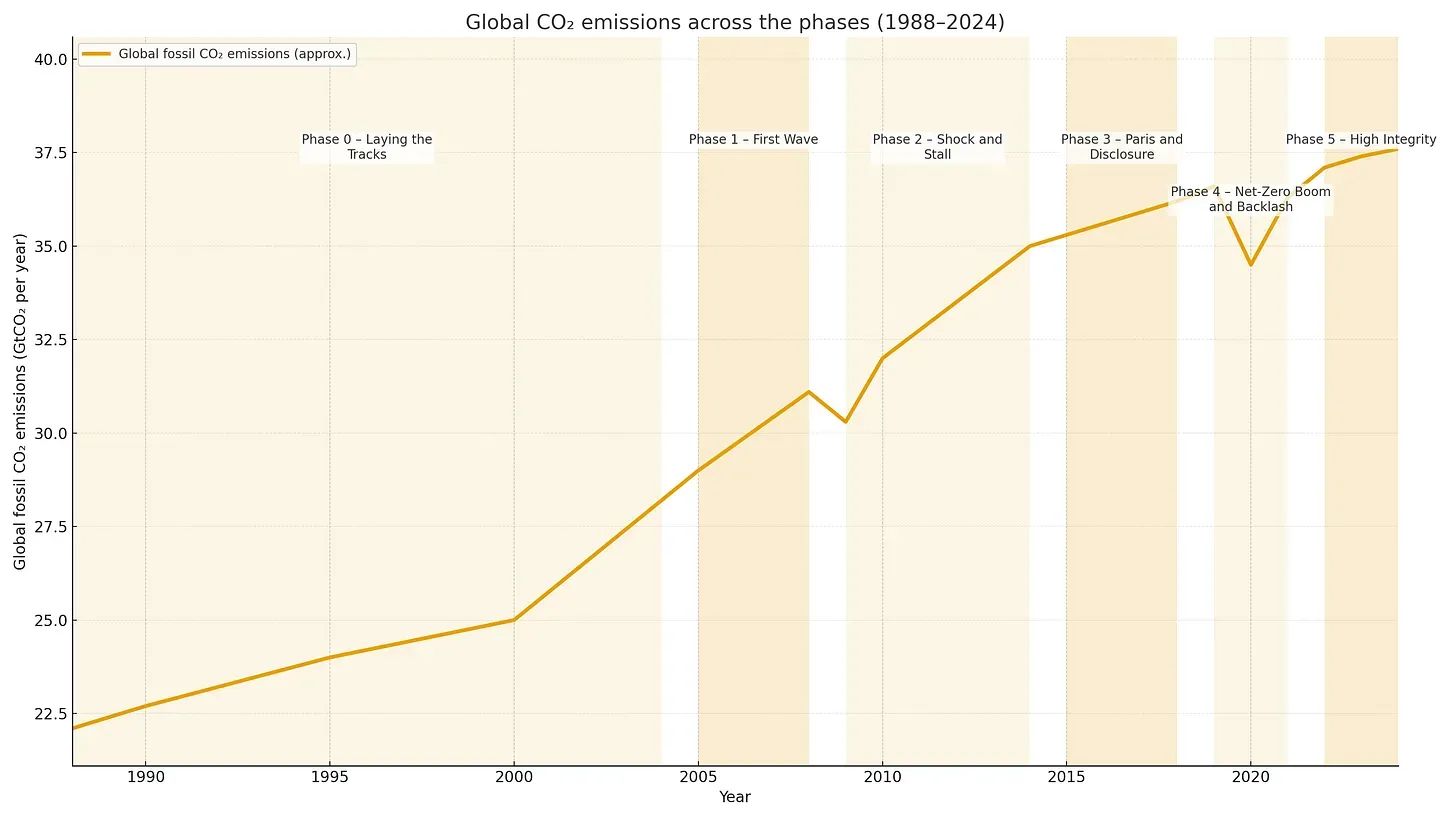

Phase 0 - Laying the Tracks (late 1980s-2004)

Before climate showed up on bills and balance sheets, it mostly lived in binders and conference rooms. Scientists nailed the physics, and diplomats set up a yearly meeting to talk about it. A first global plan (Kyoto) tried to put rules around emissions, and Europe built an early cap-and-trade prototype. Outside that, most “climate action” was small CSR projects.

- Elena (CEO, large manufacturer): “If cap-and-trade ever lands on us, we’ll adapt. Until then, keep margins.”

- Klara & Jonas, Hamburg (Germany): “Climate change? Feels like glaciers and UN meetings, not our mortgage.”

- Mauna Loa CO₂ (1988): 351.7 ppm

Phase 1 - First Wave (2005-2008)

Climate went mainstream for the first time. The EU ETS switched on. Al Gore’s documentary and a run of extreme events pushed climate into boardrooms. The early voluntary market (what we now call VCM 1.0) grew quickly with low-cost reduction and avoidance credits (renewables, industrial gases, early REDD+).

- Elena (CEO): “Buy some offsets, do the audit, show progress in the annual report.”

- Klara & Jonas: “Our power company offers a ‘green’ plan, seems cheap enough to try.”

- Mauna Loa CO₂ (2005): 380.0 ppm

Phase 2 - Shock and Stall (2009-2014)

The Global Financial Crisis and the Copenhagen disappointment took the air out. Carbon prices slumped, methodology scandals eroded trust, many buyers paused, and teams shrank. The line was “wait for clarity.”

- Elena (CEO): “Not a focus. Stabilise the business, comply, and hold.”

- Klara & Jonas: “The crisis was scary. Jonas lost his job, and we worried about the mortgage.”

- Mauna Loa CO₂ (2009): 387.6 ppm

Phase 3 - Paris and Disclosure (2015-2018)

Paris reset direction with national plans and temperature goals. Finance absorbed climate risk via TCFD and stress tests. Corporate targets matured under SBTi. MRV started to digitise with remote sensing and open data.

- Elena (CEO): “The board wants TCFD scenarios. Climate moves into real risk planning.”

- Klara & Jonas: “A letter from our pension fund about ‘climate risk’ — that’s new.”

- Mauna Loa CO₂ (2015): 401.0 ppm

Phase 4 - Net-Zero Boom and Backlash (2019-2021)

Net-zero pledges and pandemic attention drove a buying spike. Prices and volumes jumped. Then came scrutiny as investigations and NGO critiques exposed weak baselines and claims. The curve peaked, then cooled.

- Elena (CEO): “We rushed to buy tons. Now Legal is re-checking every claim.”

- Klara & Jonas: “Offsets are everywhere, and the headlines say some are junk.”

- Mauna Loa CO₂ (2019): 411.7 ppm

Phase 5 - High Integrity (2022-today)

Climate costs began to land on rich-country ledgers. Insured losses rose, heat dented productivity, and public budgets stretched. Buyers rewired for VCM 2.0 with multi-year offtakes for high-integrity removals, plus a narrow band of top-tier reductions. In Europe, CRCF, CSRD, and CBAM turned climate from virtue signal into compliance and trade. In the United States, policy swings met rising physical losses, and the costs showed up either way.

- Elena (CEO): “No more spray and pray. We sign longer contracts, and we only pay when tons arrive, backed by hard data.”

- Klara & Jonas: “We skipped sailing south because it was too hot and went to Sweden instead. It was nice.”

- Sofía & Javier (Valencia, Spain): “Water fees are up, and our city just had 50,000 people march after last year’s floods.”

- Aisha & Ben (Sonoma, California): “Our insurer wouldn’t renew. The new policy costs more and the deductible is huge.”

- Mauna Loa CO₂ (2024): 424.6 ppm

Phase 6 - The Bill Arrives (2025 →)

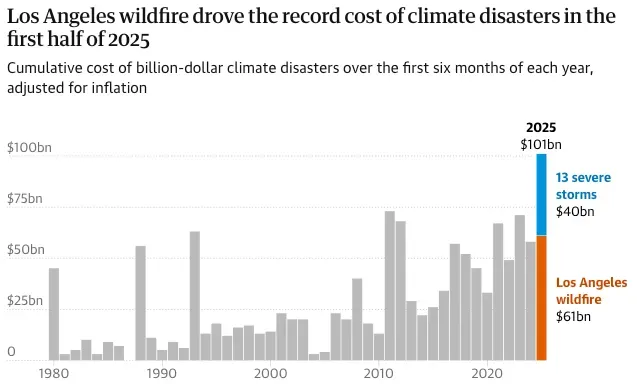

When the calendar flipped to 2025, we entered the next phase: The Bill Arrives. This summer, Europe booked a line item it did not plan for — about €43 billion in damages from heat, drought, and floods, roughly 0.26% of EU GDP in just three months. That is not “future risk”; it is today’s taxes, insurance, and prices.

For scale, €43 billion is already macro-relevant. Across the Atlantic, estimates for the Los Angeles wildfire season vary widely, roughly $100–$300+ billion depending on what you count — direct losses, health, business interruption, and rebuild. The exact figure matters less than the direction: large, recurring, and now priced into household bills, municipal budgets, and corporate risk.

What it means next

With human activity still setting new CO₂ records each year, costs go up from here. This is no longer theory. Someone pays — households, insurers, taxpayers, or firms.

We are likely entering an accountability wave. The Valencia protest last week was a real thing, and a preview. As damages mount, people will demand culprits and cash:

- Politicians for failing to act or protect.

- High-emitting companies for creating the risk and delaying fixes.

- High-consumption households (private jets, SUV fleets, mega-yachts) as symbols of unfairness.

Translation for politics and business: climate risk moves from culture war to cash war. If you cannot show real, audited climate actions, that gap becomes a legal and financial liability for boards, lenders, and insurers. Class actions and cost-recovery suits against major emitters are very likely. Directors’ duties and green claims will be tested in court, not just in headlines.

One friendly VC told me: “Real change happens when climate hits people in the Northern Hemisphere. If it happens in India, no change comes.” Brutal, but honest. We have entered that phase now. Hurricane Melissa hit Jamaica last week at Category 5, and early estimates put the cost near 30% of GDP.

Scientist’s note (Mauna Loa): CO₂ is still climbing about 2–3 ppm a year. Physics does not negotiate. Until emissions fall, the bills rise.

Bottom line: In Phase 6 you do not debate climate, you settle invoices. Either we keep paying for damage after each season, or we pay for solutions — adaptation, deep cuts, and high-integrity removals — on a schedule.

- Phase 0 - Laying the Tracks (late 1980s-2004)

- Phase 1 - First Wave (2005-2008)

- Phase 2 - Shock and Stall (2009-2014)

- Phase 3 - Paris and Disclosure (2015-2018)

- Phase 4 - Net-Zero Boom and Backlash (2019-2021)

- Phase 5 - High Integrity (2022-today)

- Phase 6 - The Bill Arrives (2025 →)

- What it means next